Line of Credit

Stay Prepared

for the Unexpected

A business line of credit ensures you have the cash flow needed to weather short-term liquidity challenges. Be ready for sudden order surges or emergencies—without disrupting your operations.

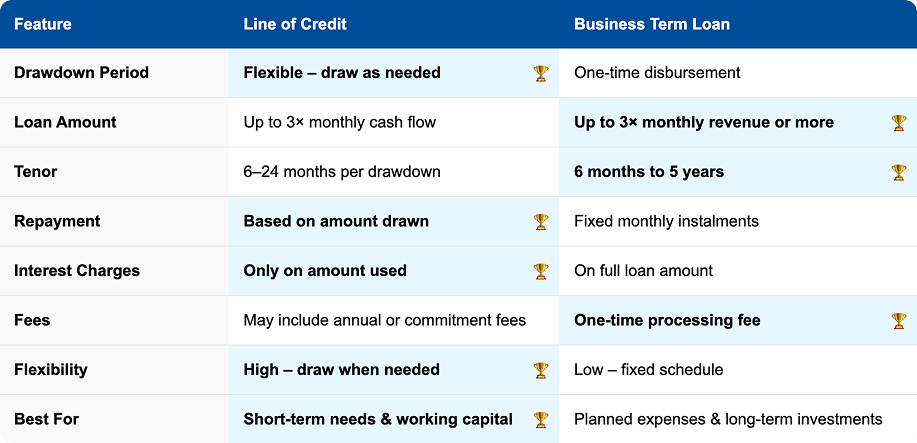

What’s the Difference Between a Line of Credit and a Business Loan?

A Line of Credit is a flexible facility that allows you to draw funds as needed, within a set limit and time period. It’s ideal for situations where the exact timing and amount of funding are uncertain—so you only borrow (and pay interest on) what you actually use.

In contrast, a Business Loan is disbursed in full upon approval, with a fixed loan amount, interest rate, and repayment term. It’s more suited for planned expenses where you know how much you need upfront.

When Is a Line of Credit Useful?

While a line of credit shares similar loan eligibility with a business term loan—often unsecured and up to 3x your monthly cash flow—the key advantage lies in its flexible access to funds. Instead of receiving the full amount upfront, you can draw down only when needed, helping you avoid unnecessary interest charges.

Here are some common situations where a line of credit proves especially valuable:

- Managing short-term cash flow gaps

- Handling seasonal fluctuations in revenue

- Covering urgent or unexpected expenses

- Taking advantage of time-sensitive opportunities

- Supporting ongoing operational needs

It’s important to note that a business term loan and a line of credit are not mutually exclusive—many businesses use both to strengthen financial flexibility and ensure they’re covered in any situation.

How Does a Line of Credit Work?

It’s simple—once you draw down on your approved credit line, it functions much like a business term loan. You’ll repay the amount through fixed monthly instalments, covering both principal and interest over a set period.

Key Things to Note:

Interest and principal are repaid monthly after each drawdown.

Terms are typically similar to a business loan, but with added flexibility on when to access funds.

While the line is pre-approved, lenders are not obligated to disburse the funds upon request. In some cases, the line may be reduced or cancelled based on changing credit risk.

For this reason, a line of credit should complement—but not replace—a business term loan, especially when funding certainty is critical.

As high as

97%*

Approval Rate

As low as

1%* / mth

Interest Rate

|

Amount

|

Up to 3x monthly cashflow |

|---|---|

|

Tenor

|

Up to 12 months |

|

Interest Rate

|

1% – 3% per month

|

|

Processing Fee

|

5% |

Our services

Other Loan We Offer